Transforming Health: Toward decentralized and connected care

This is the fifth report in the Connected World Market Insights Series.

This report is also part of the Transforming Health Market Insights Series.

Download the PDF of this report.

The big shift in Canadian healthcare: connected, integrated and community-based

The Canadian healthcare system (medicare) was established by legislation passed in 1984 and has become a hallmark of our society. Designed on the principle that healthcare is a social good and that all residents should have equal access to the appropriate medical care, the Canadian healthcare system still garners overwhelming public support.1

However, emerging challenges threaten to destabilize a healthcare system cherished by many. Over the long term, the existing healthcare delivery model will no longer be sufficient to meet the demands of the Canadian public. In order to provide the best possible care in the most affordable and efficient manner, Canada’s provinces and territories are working to modernize the way they provide healthcare products and services, an effort fueled by the ubiquitous availability of technology. In this report we investigate the two interdependent thrusts that underpin this radical transformation:

- Decentralization: Moving care outside of provider settings and into the home and community

- Connectivity: Open data sharing and communication across users and healthcare providers

Together, decentralization and connectivity have significant potential to address some of the current healthcare system’s greatest challenges and, importantly, may result in better health outcomes for citizens, while reducing the financial burden on the public purse. Successful implementation will require the combined and unified efforts of decision makers, healthcare professionals, healthcare institutions (hospitals), community-based facilities and patients. This report is part of the Connected World series and will investigate the many aspects of community-based and connected care. As Part 1, it is intended to provide background on the factors shaping the transformation of healthcare. An upcoming report (Part 2) will delve into the technologies required to successfully move care into the community and to connect all system players. Ontario entrepreneurs and researchers are hard at work developing new innovations that will fundamentally transform the existing healthcare delivery model. The follow-up report (Part 2) will highlight a selection of innovators and showcase the progress that Ontario is making.

Canadians seek better returns on their $200-billion investment

Canadians undoubtedly value healthcare and believe that it should continue to be prioritized with respect to funding.2 For Canadians, healthcare is the utmost priority (outranking education, the economy and the environment); however, in terms of performance, most feel that government’s management of our system is poor.3 Survey results show that most Canadians find healthcare to be the single most important problem facing the country.4

A 2012 study conducted by the International Centre for Health Innovation (Ivey, Western University) found that health systems in other countries are able to deliver greater value in terms of health system efficiency, life expectancy, and health and wellness than Canada, even though these countries spend less on healthcare.5 This raises the question: “Are we maximizing our return on investment in healthcare, and can our system provide greater value to Canadians?”

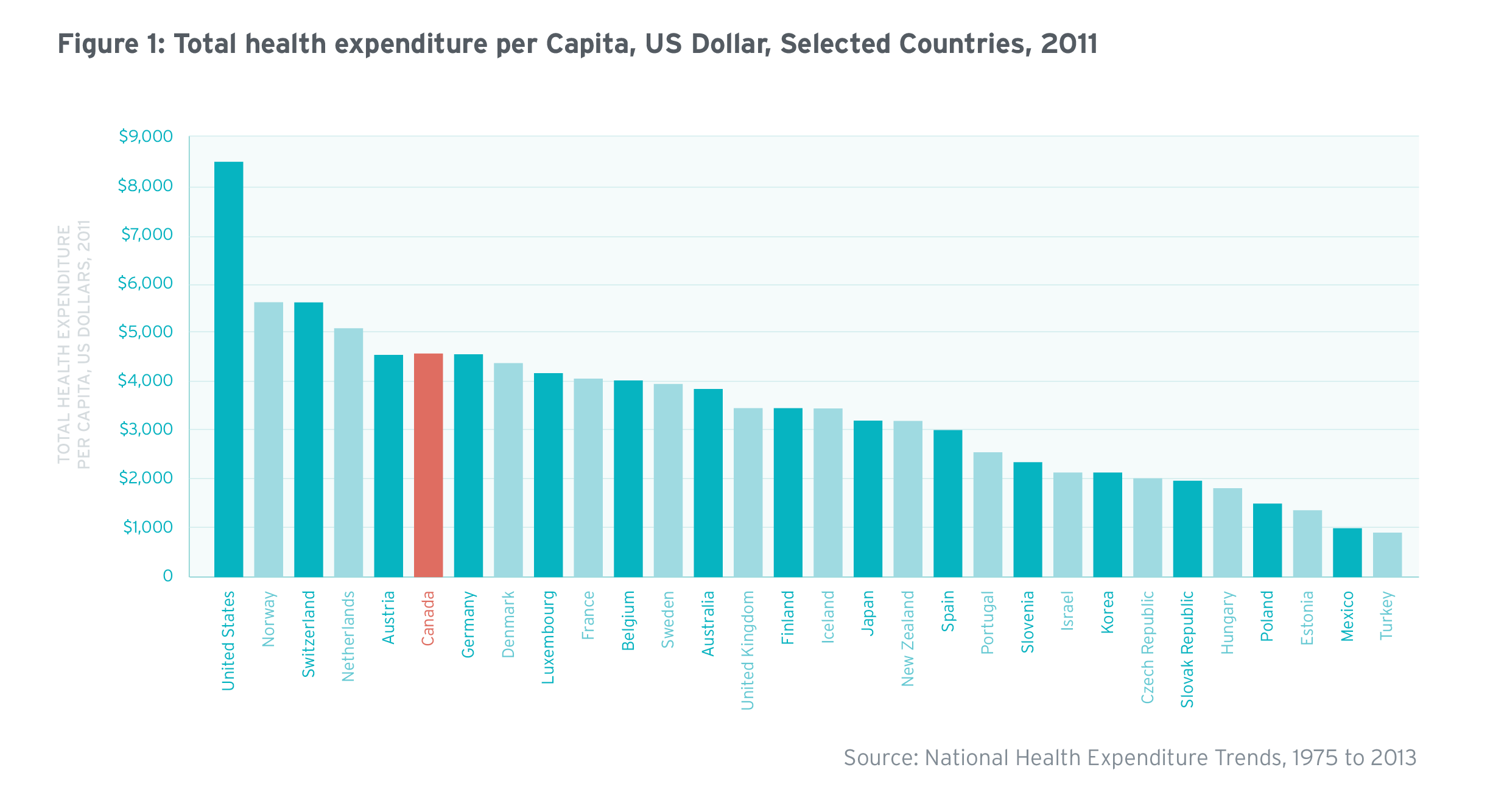

Over the last 10 years, health expenditure in Canada has increased by more than $100 billion (or 4.5% annual growth per capita6), far exceeding the country’s per capita economic growth of 0.85%7 over the same period. In 2013, total health expenditure was estimated at $211 billion, or $5,988 per person.8 Relative to peer countries around the world, Canada is one of the highest investors in health on a per capita basis (Figure 1).9 Health spending now accounts for 11.2% of GDP, up by 2 points since 2000, when it was 9.2% of GDP.10

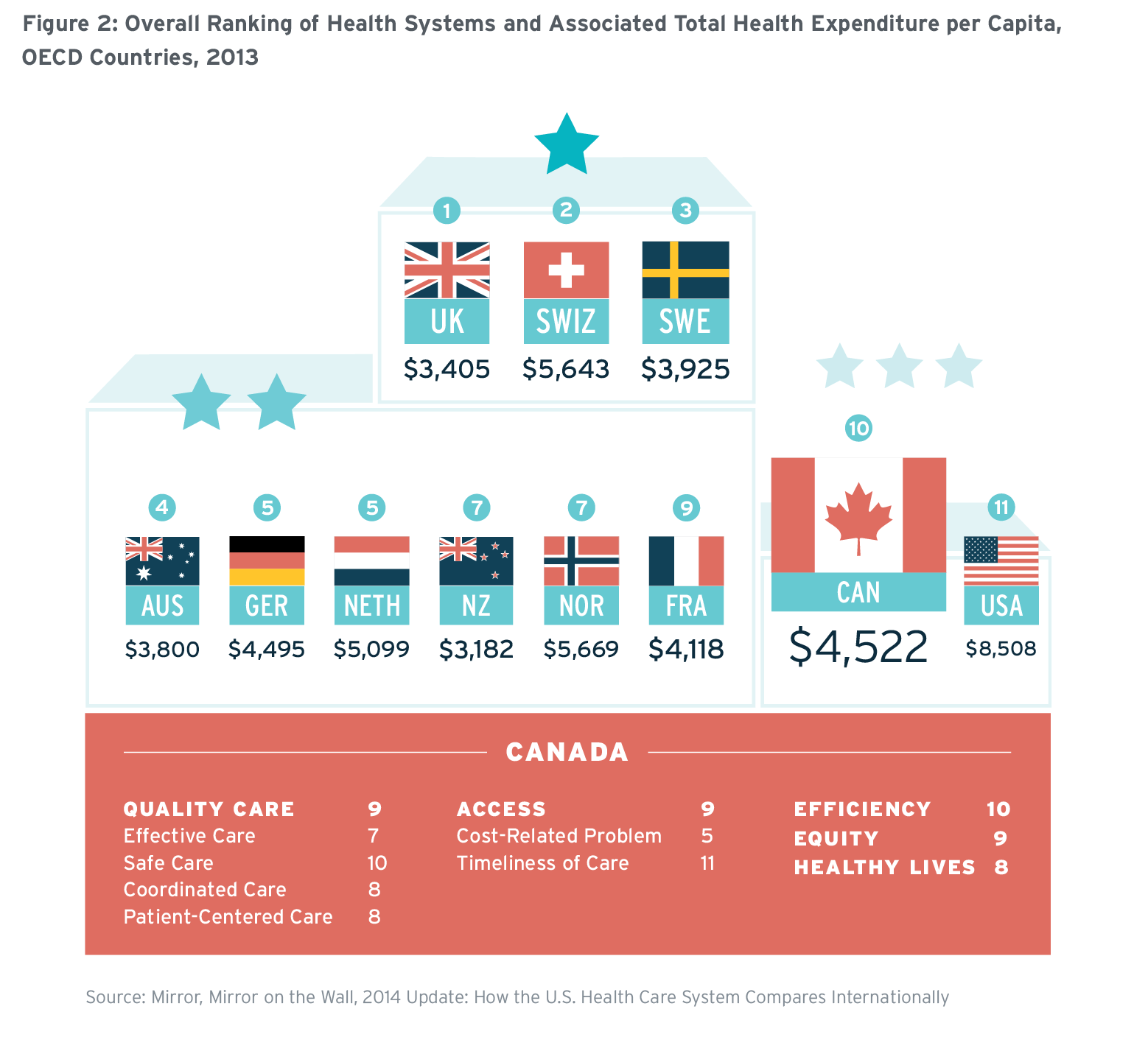

While Canada out-spends most of its peers in terms of healthcare investments, this has not necessarily translated into better results for Canadians’ health. A recent study conducted by the American healthcare think-tank the Commonwealth Fund ranks Canada’s healthcare system tenth out of 11 peer OECD countries (Figure 2).11 Canada only ranked higher than the United States. The United Kingdom ranked first overall, despite the fact that the country spends only $3,405 per capita, approximately $1,000 less per person than Canada.12 Based on such studies, many have argued at a macro level that our current healthcare system is not working as effectively or efficiently as it could.

A healthcare system under pressure

Like many jurisdictions around the world, Canada faces complex healthcare challenges. Here, we highlight four challenges that are putting pressure on the current healthcare paradigm—the first two are largely population driven, while the latter two are system driven. Those challenges are: 1) managing the ubiquity of chronic illness; 2) caring for an increasingly aging population; 3) the increasing cost of labour; and 4) the adoption of new medical technologies.

1) Ubiquity of chronic conditions

According to the World Health Organization chronic, “incurable” illnesses (or non-communicable diseases) are the leading cause of mortality worldwide and are directly responsible for 63% of all deaths annually.13 In addition to having a serious impact on health (morbidity), chronic illnesses also have a profound economic burden to society, both in terms of healthcare costs and productivity losses.14 In 2010, 58% of annual healthcare spending ($68 billion) was for the treatment of incurable illnesses. The indirect costs, which include income and productivity losses, amounted to $122 billion.15

This burden of chronic illness is not only high, but it is also growing. In Canada, chronic disease is estimated to now account for 88% of total deaths.16 Furthermore, 40% of Canadians aged 12 or older have at least one chronic disease and 80% are at risk of developing a chronic disease.17 The crux of the challenge is finding a way to manage multiple chronic conditions, as our healthcare system was designed to address single episodic issues, not complex chronic conditions. More than 25% of Canadians now report having two or more chronic conditions.18

Chronic illnesses are nearly preventable, as they are caused mostly by behavioural and lifestyle choices. Maintaining a healthy diet, getting physical exercise, abstaining from tobacco use and not consuming harmful amounts of alcohol can prevent approximately 80% of cases of heart disease, diabetes and respiratory diseases, and 40% of cancers.19 Despite this fact, 50% of Canadians are not consuming enough fruits and vegetables, 50% of adults are not getting enough exercise, 20% of Canadians are smokers and 5% consume alcohol on a daily basis.20 This supports the notion that community programs targeted at changing personal behaviour can have great impact on reducing the devastating effects of chronic illness, both on a social and an economic level.

Despite the overall increase in healthcare expenditure, Canada lags behind other nations in providing the appropriate infrastructure and support for people living with one or more chronic conditions.21

2) Caring for an aging population

Canadian citizens aged 65 and older represent 14% of the population, however, they consume nearly 45% of government healthcare spending.22 Compared to the national average of $5,988 per person per year, seniors aged 65 and older require $11,794 per year in healthcare resources, while Canadians aged one to 64 require $2,341 per year.23 As seniors age, their need for healthcare products and services increases significantly. The per capita cost of care for older seniors aged 80 and older is $20,387, which is approximately three times greater than the per capita cost of care for younger seniors, aged 65 to 69 ($6,431 per year).24 One of the primary reasons that healthcare is more expensive for seniors is that many are living with chronic conditions; in fact, approximately 75% of Canadian seniors are living with one or more chronic condition.25 Furthermore, a study conducted by the Canadian Institute for Health Information (CIHI) found that the most important contributing factor for the level of healthcare use by seniors was the number of chronic conditions they had, and not their age.26 For instance, seniors with three or more chronic conditions use 40% of all healthcare used by seniors, even though they only represent 24% of all seniors.27

Our healthcare system was not designed to provide healthcare to a population of seniors who would live into their eighties, often with multiple chronic conditions. The solution to caring for an aging population lies in how and where care is provided to seniors.

3) Increasing cost of labour

Over the last 10 years, the predominant driver of healthcare spending has been the compensation of healthcare professionals.28 Hospitals account for 30% ($62.6 billion) of total healthcare expenditure.29 Within this, salaries constitute 60% of total hospital costs.30 Compensation of healthcare workers in hospitals has outpaced compensation in non-health sectors.31 Similarly, expenditure on physicians in the community has also been increasing, due to the increased number of physicians and rising salaries.32 From 1998 to 2008, total public sector spending on physicians has increased at an annual rate of 6.8%.33 The main driver during this time has been increases in physician fees, which have grown faster than compensation for other healthcare professionals.34

The high cost of labour in the healthcare system can be partially attributed to the fact that, unlike other labour-intensive industries, technological innovations in healthcare in general have not greatly reduced the need for (or cost of) labour.35 In fact, in many cases novel technologies further amplify the need for human labour,36 largely because new technologies require skilled professionals to operate them.

There are some instances where health technologies can increase productivity and reduce labour-associated costs. Good examples of these types of innovations are modern health-IT type technologies that reduce or eliminate the need for administrators and other healthcare professionals.37 Interestingly, it has been emerging countries that have been quick to adopt health-IT technologies, primarily because of shortages of skilled labour.38 For example, in Mexico and India, healthcare has moved from the hospital to the home through the use of telemedicine services.39 These services are relatively inexpensive and provide care in an efficient and effective manner.

4) Adoption of new medical technologies

Technology’s role in healthcare delivery is a major driver of the inflation of healthcare spending. Canadians now undergo more innovative medical procedures that leverage new technologies, and consume more drugs than they did when the health system was initially designed (as many of these advances had not yet been invented/discovered or were not yet widely available at that time). In fact, in 2011, Canada had the second-highest expenditure on drugs per capita among OECD countries.40

On one hand, the direct costs of the Canadian health system adopting these new technologies have been shown to be a key driver of inflation.41 On the other hand, many argue that the reason new technologies drive healthcare inflation is that the full impact of these technologies on reducing demand for health resources is never realized upon their introduction. That is, we are adding new costly technologies—the results of decades of investments in biomedical research—to a system that is fundamentally broken in its design, leading to a “more expensive broken system” instead of a better operating system. Michael Porter, a professor at Harvard Business School and one of the world’s foremost thought leaders on transforming healthcare, summarizes this issue nicely: “Today, twenty-first century medical technology is often delivered with nineteenth-century organization structures, management practices, measurement methods, and payment models.”42 Our healthcare system needs to be redesigned in order to reap the full benefits of advanced medical technologies, which will result in a more efficient system.

A way forward: two innovative strategies

Given the current state of our healthcare system and the future health needs of Canadians, maintaining the status quo is not an option. Jurisdictions across Canada are looking to significantly change how healthcare products and services are designed, delivered and paid for, particularly as costs driven by the aging population, chronic disease and adoption of advanced technologies become more burdensome.

Canada (and its peers around the world) are pursuing two common strategies to help address the growing strains on existing health systems:

A. Community-based healthcare: Decentralizing health care by moving care out of resource-intensive institutions (such as hospitals), and into models of care delivery and even self-management in the home and community

B. Connected healthcare: Using healthcare information technologies and processes to “Connect all parts of a healthcare delivery system, seamlessly, so that critical health information is available when and where it is needed”43

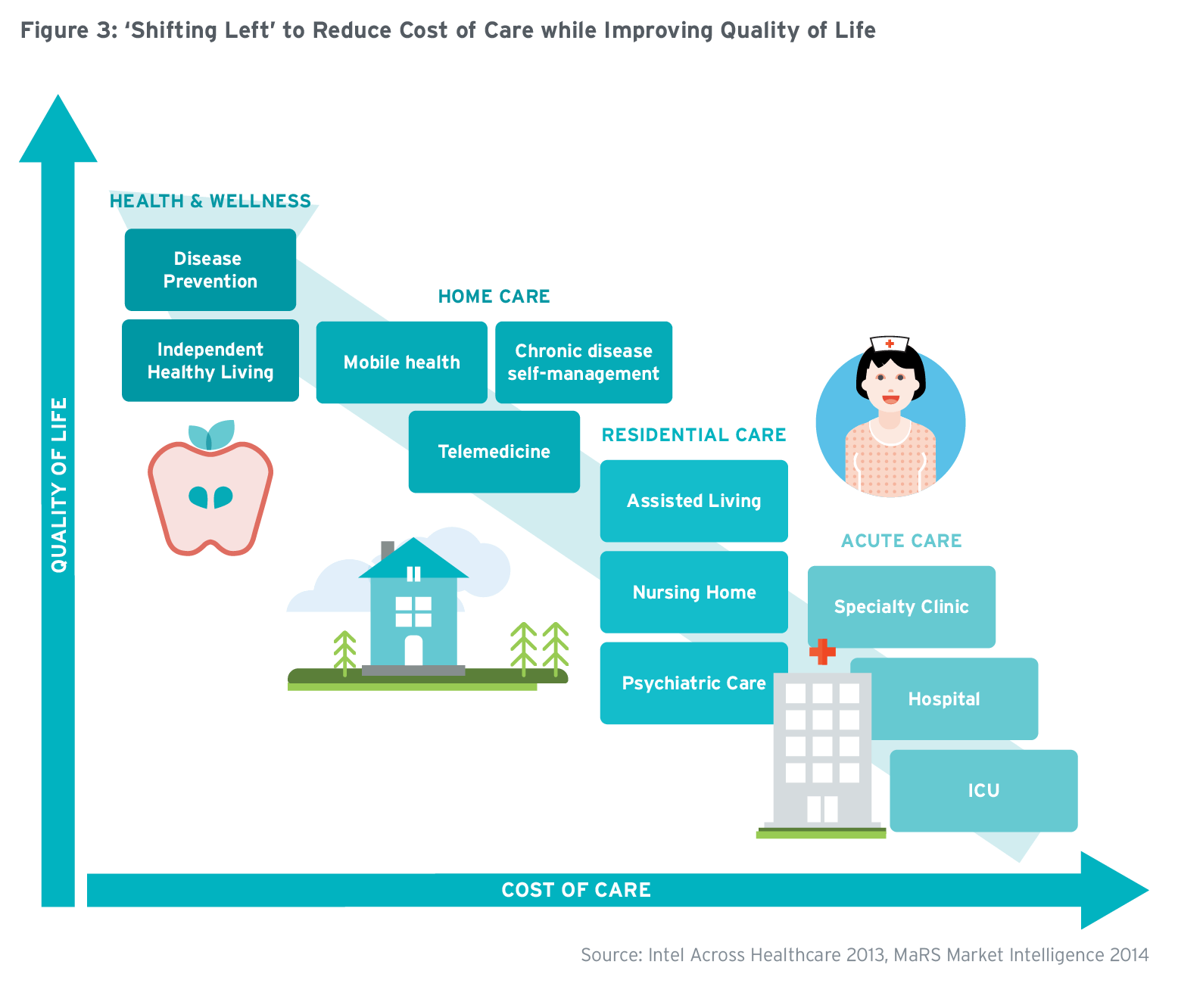

Shifting left: moving toward community-based healthcare

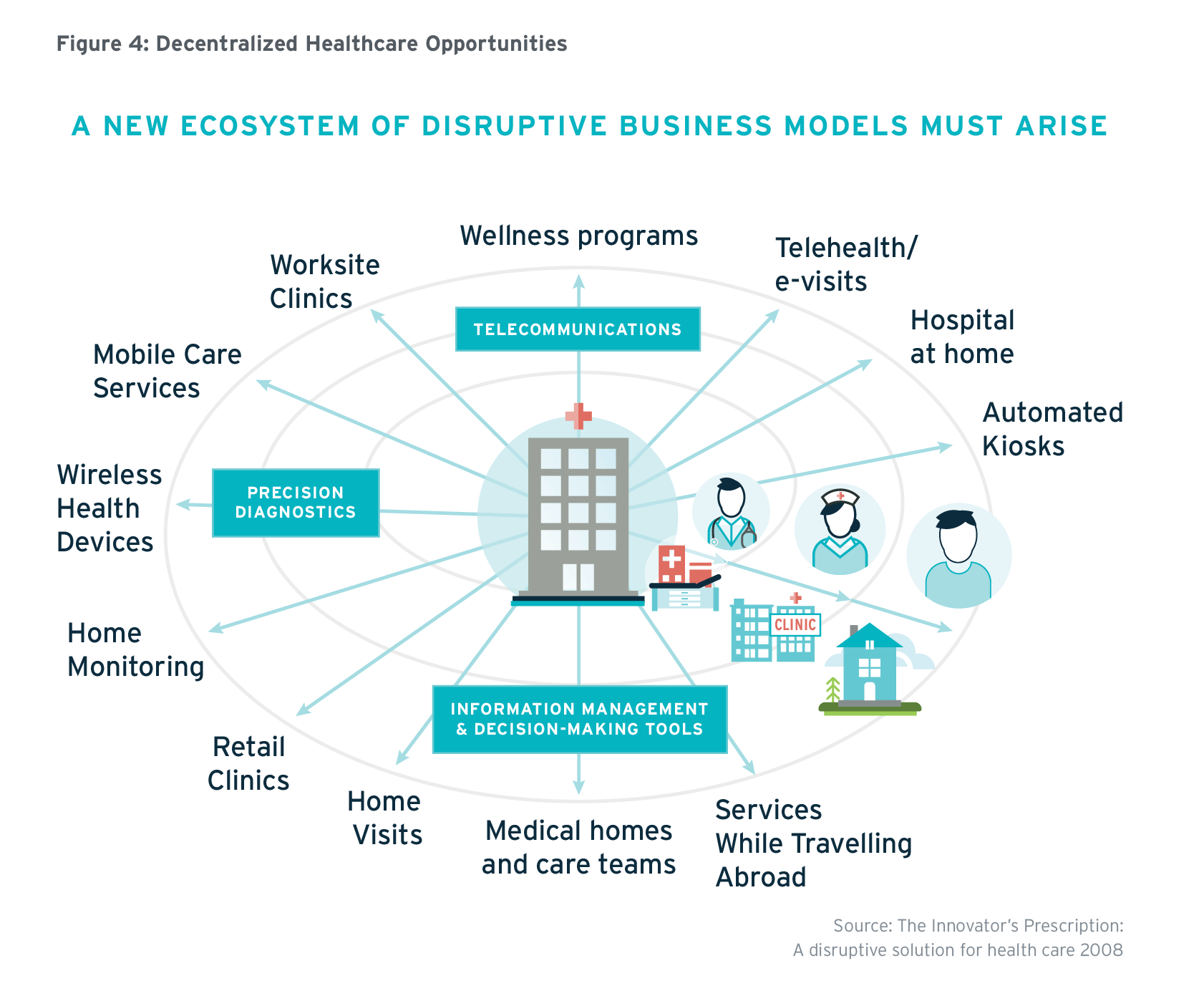

Healthcare delivery has traditionally been designed around the provider, located in institutions such as hospitals, clinics or doctors’ offices. In place of formal, institutionalized care, health systems are now making a more patient-centric “shift left” (Figure 3) toward settings where the care goes to the patient, instead of the patient going to the care.44 These new settings may include a patient’s home, community health centre, school or workplace, and many more locations convenient to citizens, such as retail shops (Figure 4). Some regions are even trying mobile units45 that move around the community, providing care where and when needed. This responsive model provides more flexibility than the capital-intensive, bricks-and-mortar, institution-centred approaches. Though these may seem like non-traditional locations to deliver healthcare, in many cases they are already the preferred destination; for example, flu vaccinations provided at the workplace or local pharmacy, wound care provided at home by a visiting nurse, diabetes nutrition education provided at a local community centre and so on.

Services in the community that can affect health are also in play. It has been well documented that many other social and environmental factors work together to affect a person’s health and ultimate need for healthcare services.46 As a result of this research, health systems are increasingly investing in programs, services and resources that aren’t commonly considered part of the formal medical care system, in order to reduce the demand for healthcare services downstream. For instance, improving sidewalks and pathways in a neighbourhood can encourage pedestrian and cyclist usage, thereby increasing physical activity and decreasing the risk of community members developing or advancing chronic disease.47

By shifting healthcare and illness-prevention services outside traditional bricks-and-mortar healthcare delivery locations, patients, providers and the health system itself can reap a number of benefits that include, but are not limited to, the following:

Benefits achieved by moving care to the community

| Benefit of decentralizing healthcare | Evidence |

| Increased patient comfort and ease | Many individuals experience anxiety and discomfort when visiting a doctor or hospital. This can affect more than simply their emotional well-being: Studies show that 20–25% of patients with high blood pressure are actually suffering White Coat Syndrome, a phenomenon where doctor- or clinical setting–related anxiety induces an acute increase in blood pressure.48 Using new technologies to provide healthcare in an informal community setting and having allied healthcare professionals provide the care may help to put more patients at ease. Leveraging community settings and less trained staff can also greatly improve access to care, especially for vulnerable populations who face barriers to accessing formal medical models of care (such as geographic distance or literacy problems) and can also reduce wait times. |

| More convenience and greater sense of independence and control | By leveraging technology and alternative caregiving staff, seniors and individuals with complex illnesses are able to access healthcare on their terms. For one, they can remain in their own homes and communities and behave more like partners in managing their own health. In doing so, these individuals could increase their self-worth, reclaim control (formal health systems are characterized by many as paternalistic, done “to you” instead of “for you” or “with you”) and foster their sense of independence.49 |

| Better models for managing chronic conditions | Chronic conditions, such as diabetes, must be managed 24 hours a day, seven days a week, 365 days per year.50 Community care is a more logical approach for chronic disease management and self-management because it allows for more continuous interventions, rather than episodic interventions that only occur when the patient visits their formal care provider. There is a growing body of evidence that supports the positive impact of integrating traditional and community-based healthcare for management of chronic conditions such as diabetes, hypertension, obesity and frailty in the elderly.51 |

| Improved health outcomes | Researchers have studied community care and its integration with existing formal care resources, and have determined that, generally speaking, patients fare better when cared for outside of institutions (under non-acute conditions). Programs leveraging community-based care have been shown to help patients with congestive heart failure, asthma, diabetes and other conditions to reduce hospital readmissions/emergency visits, improve quality of life, decrease HbA1C and achieve other positive improvements to their health.52 |

| More compassionate end-of-life-care | Currently, most terminally ill and elderly patients pass away in a hospital.53 It would be much more compassionate to provide end-of-life care at home or in the community, which the majority of these patients have expressed as the preferred setting for their final moments.54 |

| Increased focus on prevention and proactive care | Due to the resources at hand, community care is often focused on early intervention, especially for those who are “at risk,” in order to keep the population healthy. This may mean primary prevention (stopping you from getting sick in the first place) or secondary prevention (stopping chronic diseases from advancing to devastating complications). Shifting focus to this type of proactive care is not only of great benefit to the health system (frees up resources for those who need them), but is also beneficial to patients and their families because it reduces the occurrence of acute episodes requiring hospitalization, thereby decreasing stress, improving the patient experience and lessening the chance of acquiring infections in hospital.55 |

| Lower service cost | Hospital infrastructure and highly skilled professional labour (physicians, nurses) are costly and in limited supply. When acute care is not required, it is best to avoid these costly service options, instead using less capital- and resource-intensive settings (for example, homes, workplaces, malls and community centres) and leveraging staff with the minimum sufficient skills (such as personal support workers, occupational therapists, physical therapists and midwives). In many cases, this allows the health system to provide the same or improved care at a lower cost. |

With these benefits in mind, many health systems worldwide are now shifting care into the community. Some notable examples of successful interventions include:

| Stage | Intervention | Description |

| Healthy | Northland Emergency Meningococcal C Vaccination Programme (NZ)56 | Introduced in response to a 2011 outbreak, vaccinations were promoted and delivered by the public health service, primary health providers, Maori service providers, schools, general practice clinics, community clinics and outreach home-based vaccination services. The program successfully vaccinated 73% of the targeted population. |

| Health at risk/Worried well | txt2stop Smoking Cessation Program (UK)57 | Smokers were sent text messages of behavioural-change support to encourage smoking cessation. After six months, participants were significantly more likely to have quit smoking. |

| Unwell/Sick | Wound Healing Community Outreach Service (AUS)58 | Clients accessed the nurse practitioner–led community-based wound clinic on an ongoing basis, without need for a referral. Clients received treatment, peer support and prevention strategies in an informal environment. The program resulted in 90% of leg ulcers healing within 24 weeks (a two-week reduction). |

| Chronically unwell | Diabetes Health: It’s In Your Hands (US)59 | Type 2 diabetics had access to one-on-one (home) or group (community) sessions led by paraprofessionals on goal setting, problem solving, and learning-, movement- and food-related activities. After 10 weeks, participants had significantly improved their HbA1C, BMI, smoking habits, fruit/vegetable intake, and appraisal of diabetes scores. |

| Palliative (end of life) | Silver Chain Community-based Palliative Care (AUS)60 | Adults with cancer were given early access (90+ days prior to death) to community-based palliative care. This group was significantly less likely to visit an ER, and was thereby able to avoid the associated stress. |

Like its peer jurisdictions across Canada and around the world, Ontario has also elected to focus on community-based healthcare. Ontario’s Action Plan for Health Care61 outlined three primary goals:

- Keeping Ontario healthy

- Providing faster access and a stronger link to family healthcare

- Delivering the right care, at the right time, in the right place

Each of these goals is underpinned by community-based care delivery models, including smoking cessation guidance through local pharmacists, nurse house calls for frail seniors and deep investments in home care provided by personal support workers. The action plan also highlighted some of Ontario’s existing successes with respect to community-based care, such as:

- Kensington Eye Institute: A community clinic that performs cataract procedures in a “factory-focused” model, moving the procedure out of the traditional, costly hospital setting and into the community, where it is closer to the patient, faster and significantly less expensive

- Ontario Telemedicine Network: Building infrastructure across Ontario to allow patients to remotely access the province’s specialists, who currently reside only in major urban academic medical centres

Ontario will confront a number of challenges as it moves forward with implementing increased community-based care.

| Challenge | Description |

| Existing hospital- and physician-centric paradigm | As noted above, and similar to most health systems in the world, Ontario’s health system was designed around a provider-centric paradigm. Through legacy policy and funding, these institutions and professionals wield significant decision-making power and influence. As a result, current (and likely future) healthcare initiatives usually take place within facilities, and the role of physicians is greatly emphasized.62 Yet, most agree, “A health care system should, first and foremost, be organized to meet the needs of patients, rather than the needs of institutions and providers.”63 Only when the dynamic is shifted, empowering community-based providers and providing the necessary funding, will Ontario be able to effectively move care into the community. This will require significant policy and structural reform, as well as change management at a high scale. Encouragingly, progress is already being made. In 2012–2013, 308,000 patients received patient-centric community-based care through the Ontario Telemedicine Network,64 and the program’s CEO predicts, “by 2020, 25% of health[care] will be delivered virtually.”65 |

| Complexity of care co-ordination | When care is spread between different locations and providers, it’s difficult to ensure the patient is receiving optimal care that meets theirneeds. Without a more integrated approach, “patients can get lost in the system, needed services fail to be delivered or are delayed or duplicated, the quality of the care experience declines, and the potential for cost-effectiveness diminishes.”66 Ontario’s current system, particularly with respect to palliative home care, has been described as “a patchwork of independent players in which neither the payer nor the providers are directly accountable for health outcomes or for resource consumption.”67 In the future, improved care co-ordination will depend upon the use of electronic medical records (EMRs),68 electronic health records (EHRs), secure communication tools and other technologies, and will require protocols allowing the sharing of personal health information between providers within a patient’s circle of care. |

| Availability of relevant and timely health information | Healthcare, like most knowledge-economy sectors, is about communicating information and acting on that information. The vast majority of healthcare providers now keep some form of digital medical record (70% of Ontario physicians use an EMR in their practice),69 but a record on its own is not enough to ensure the best care, particularly if there is no effective means of sharing the information it contains with the people who can make decisions based on that information (that is, patients and their formal and informal caregivers). Even within the same provider, for example, a hospital, “important information often remains siloed within one group or department because organizations lack procedures for integrating data and communicating findings.”70 This challenge is made more complex due to concerns surrounding data privacy and security. Many efforts are underway to put measures in place to ensure the “appropriate use of data for health system decision-making,”71 by preventing unnecessary access while also facilitating access for those who need the information. Most importantly, to continue the transformation toward patient-centricity, systems to capture patient consent must be used to guarantee, “patients’ wishes are followed regarding the secondary use of their personal health information.”72 Most experts agree that these challenges are difficult, but are not the bottleneck to progress. The more salient barriers are around workflow and technical challenges. Within internal medicine, workflow-related factors such as “policies and procedures, inefficient processes, teamwork, and communication,” contributed to diagnostic error in 65% of cases.73 Changes to these factors will require careful workflow re-design, the adoption of which may depend heavily on workplace culture and physicians’ willingness to stray from tradition. From the technical perspective, records kept by one provider are often in a format incompatible with others’ systems. Moving forward, technologies must be “designed for interoperability, using common approaches and content standards, to enable health system use of data.”74 Once these challenges are addressed through policy and technology, providers will have the information they require to provide the best care. |

| Capacity | [inlinetweet prefix=”” tweeter=”” suffix=”We can make the shift.”]Currently, the demand for community-based care outweighs the supply:[/inlinetweet] only 6% of Ontario’s $45 billion in healthcare spending is dedicated to community care, while almost 35% is put toward the operation of hospitals.75 As a result of this imbalance, Ontario relies upon expensive alternative level of care (ALC) hospital beds, where patients remain until they are admitted elsewhere.76 Moving care into the community will not be possible until the necessary community resources (facilities, staff, supplies and technology) are identified, funded and put in place. |

Connected healthcare

Many of the initiatives and challenges above share a common theme: the availability of data, and its effective communication and use. Achieving a system that is integrated with community-level assets requires information to flow to all providers in an individual’s circle of care (hospitals, clinics and third parties such as home-care providers and informal care providers). Service between care providers can be co-ordinated through connectivity, allowing for seamless collaboration.

Ontario is increasingly focused on improving health-IT infrastructure and policies relating to the digitization of data from across the system, and how that data is used, collected, communicated and acted upon. In doing so, Ontario will ensure the required connectivity tools and information are available to those providing care throughout the province’s communities.

Achieving a connected healthcare ecosystem

The digitization and connectedness of health system data is a major priority for Ontario and health systems around the world. There are three key elements required to ensure access, collection and sharing of information across parties:

- Electronic medical records (EMRs)

- Consumer involvement

- Data and analytics

For connected health to become a reality, seamless interoperable [inlinetweet prefix=”” tweeter=”” suffix=””]health data must flow bidirectionally between individuals and their care providers in real time[/inlinetweet].

1. Role of electronic medical records in connected health

A core system-level asset in connected health is the electronic medical record (EMR) maintained by healthcare providers, which allows primary care providers to capture and store patient information. Data elements within an EMR can include patient demographic information, diagnosis, lab results, medication, medical history and many others. Supporting solutions include clinical decision support systems (CDSS), computerized physician order entry (CPOE), and specialized systems, such as picture archiving and communication system (PACS) for storage and access of medical images, and laboratory information management systems (LIMS) for use in laboratory settings. Health information exchanges (HIEs) or repositories bring together the plethora of provider-based digital health data sets to allow ubiquitous access to health information from different vendors, providers and sometimes patients, often across different locations. For HIEs to be effective, the software must follow specific standards that enable the communication between the constituent pieces of software. In Canada, Canada Health Infoway (CHI) detailed the health information access layer (HIAL) standard that all HIE software in the country must use.

2. Role of the consumer in connected health

From the perspective of the citizen, the building blocks of connected health include digital health technologies such as:

- Personal health records (PHRs)

- Patient portals

- Mobile health and medical apps

- Communication tools and social networks

- Wearable technologies and sensors

These consumer digital health technologies consist of tools used outside of traditional medical settings, leveraging data found in the formal healthcare system (for example, in the EMR), to increase engagement with a person’s circle of care, in order to better track and manage their health. These technologies also carry the potential to redefine how a patient’s formal healthcare team can seamlessly keep abreast of their patient’s health status, and work together proactively to keep them healthy. For example, in the near future, the concept of scheduling an annual check-up will be outdated.

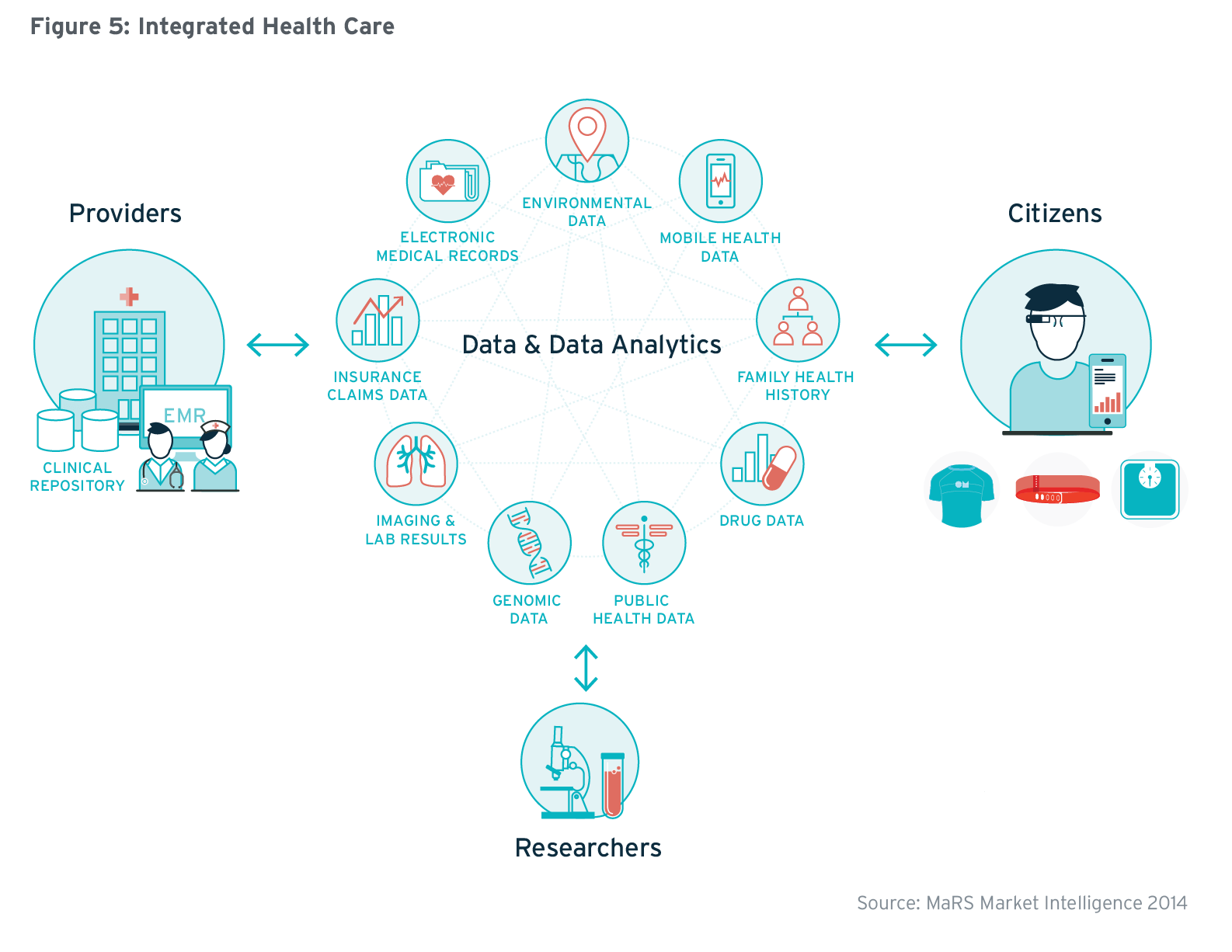

3. Data and data analytics become central figures in a connected health paradigm

Digitized medical data is a tremendous asset and vital currency for connected healthcare. With the onslaught of new consumer digital health tools and devices, there is now an abundance of unstructured, patient-generated health data available, in addition to existing, more structured health-related data. This includes health history, symptoms, biometric data, treatment history, lifestyle choices and other information—created, recorded, gathered, or inferred by or from patients or their designees (that is, care partners or those who assist them) to help address a health concern.77 Further still, a flood of other molecular, genomic, environmental, behavioural and social/contextual data is more available and accessible than ever before. When combined, these data sets form the basis of “Big Data” in healthcare, so called not only for its sheer volume but also for its complexity, diversity and the speed at which it grows.78

Data analytics brings it all together, completing the connected health ecosystem. Analytics, and the applications that make the data actionable, will ultimately transform healthcare by enabling decisions to be made by each of the members in the full circle of care around an individual. This will help Ontario reach its goal of providing the right care for the right patient at the right time—for the right price.

The value of connected health

Enabling the shift toward community-based healthcare only skims the surface of the value and benefits of connected health. Below is a summary of additional ways that connected health affects stakeholders in Canada’s health ecosystem.

| Ecosystem stakeholder | Value of connected health | Select examples |

| Citizens | Citizens are more engaged with their healthcare providers and more motivated to self-care. They can easily book appointments, check their health status, track and send data to their provider, and verify medication and vaccination records. | In the US, citizens are downloading their personal health records from multiple care providers using the Blue Button initiative. Blue Button is now machine-readable, so that mobile apps can leverage the standard to help patients track and manage their disease. |

| Healthcare organizations and systems | Connected health enables the creation of integrated health systems—seamless co-ordinated care across the system from any partner. It is also allows for system-wide performance measurements and allows organizations to “compete” for best results. | At Odense University Hospital, in Denmark, a connected health platform allowed the hospital to care for patients remotely, while patients stayed home. Patients with COPD allowed monitoring and care, resulting in lower readmission rates (by more than 50%), shortened hospital stays and better patient satisfaction and quality of life.79 |

| Health professionals | Connected health information allows physicians to spend less time looking for information and more time on what matters: treating the patient. With real-time access to patient data through EMRs, HIEs and PGHD, physicians can more accurately diagnose disease, treat and follow-up with patients. | American managed care consortium Kaiser Permanente “developed a Panel Support Tool linking evidence-based care guidelines to its EMR, highlighting gaps in care for individual patients and ultimately improving treatment outcomes.”80 |

| Researchers and innovators | Connected health can augment insight derived from clinical trials. It can also aid in personalized medicine research. | The EMR used by Kaiser Permanente provided the data that led to the discovery that Vioxx had significant adverse drug effects81 (serious coronary heart disease, fatal in 27% of cases).82 This led to the subsequent withdrawal of the drug from the market. |

| Civil society | Connected health data can be used to ensure rapid, co-ordinated detection of infectious disease. It can also allow citizens to effectively measure the efficacy of their health systems, facilitating policy changes based upon scientific facts. | Toronto-based BioDiaspora uses Big Data analytics, including global air traffic patterns data, to predict the international spread of infectious disease. The BioDiaspora platform has been used by numerous international agencies, including the U.S. Centers for Disease Control and Prevention, the European Centre for Disease Prevention and Control, and the World Health Organization. |

Looking ahead: the path to an integrated, community-based health delivery model

The shift toward integrating the delivery of healthcare services in the community with traditional formal care holds great promise to improve citizens’ health while keeping costs under control. Realizing these benefits entails a transformative innovation agenda, which will require Ontario to activate all levers of the health ecosystem.

- Citizens: Greater engagement, activation and willingness to self-manage where education and other resources are provided

- Health providers: Openness to change workflows and decision-making processes to incorporate greater volumes and types of data, as well as a willingness to adopt new technologies that will improve connectivity, communication and co-ordination in order to enable a “shift left,” but that may also disrupt traditional hierarchy

- Innovators: New technologies that leverage health data and enable community-based care to improve outcomes and reduce costs through decreased labour and physical overhead

- Government: Policies that allow for the creative destruction of legacy institutions that no longer serve the health needs of the population, and policies that nurture and encourage innovators to create health-IT solutions where information flows openly (yet securely) to required parties

There is significant activity underway by each of these constituents of the Ontario health system. The next health-focused report in the Connected World Market Insights Series will concentrate upon the role of Ontario’s entrepreneurs in developing innovations that will fundamentally transform how (and where) healthcare is delivered in Canada.

[download url=”https://www.marsdd.com/wp-content/uploads/2014/09/Sep15-MaRS-Whitepapers-SmartHealth.pdf” type=”pdf”]Transforming Health: Towards decentralized and connected care[/download]

References

1. McBane, M. Canadian Health Coalition. (2011). “Support for public health care soars: 94% of Canadians—including Conservatives—choose public over for-profit solutions.” Retrieved from http://www.newswire.ca/en/story/884001/support-for-public-health-care-soars-94-of-canadians-including-conservatives-choose-public-over-for-profit-solutions

2. Saroka, S.N. (2007). Canadian Perceptions of the Health Care System. Retrieved from http://www.queensu.ca/cora/_files/PublicPerceptions.pdf

3. Saroka, S.N. (2007). Canadian Perceptions of the Health Care System. Retrieved from http://www.queensu.ca/cora/_files/PublicPerceptions.pdf

4. Saroka, S.N. (2007). Canadian Perceptions of the Health Care System. Retrieved from http://www.queensu.ca/cora/_files/PublicPerceptions.pdf

5. Snowdon, A., Schnarr, K., Hussein, A. & Alessi, C. (2012). Measuring What Matters: The Costs vs. Values of Health Care. Ivey International Centre for Health Innovation. Retrieved from http://sites.ivey.ca/healthinnovation/files/2012/11/White-Paper-Measuring-What-Matters.pdf

6. Canadian Institute for Health Information. (n.d.) National Health Expenditure Trends, 1975 to 2013. Retrieved from https://secure.cihi.ca/free_products/NHEXTrendsReport_EN.pdf

7. The World Bank. (n.d.) GDP per capita growth (annual %). Retrieved from http://data.worldbank.org/indicator/NY.GDP.PCAP.KD.ZG

8. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

9. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

10. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

11. Davis, K., Stermikis, K., Squires, D. & Schoen, C. The Commonwealth Fund. (2014). Mirror, Mirror on the Wall. Retrieved from http://www.commonwealthfund.org/~/media/files/publications/fund-report/2014/jun/1755_davis_mirror_mirror_2014.pdf

12. Davis, K., Stermikis, K., Squires, D. & Schoen, C. The Commonwealth Fund. (2014). Mirror, Mirror on the Wall. Retrieved from http://www.commonwealthfund.org/~/media/files/publications/fund-report/2014/jun/1755_davis_mirror_mirror_2014.pdf

13. World Health Organization. (March 2013). 10 facts on noncommunicable diseases. Retrieved from http://www.who.int/features/factfiles/noncommunicable_diseases/en/

14. Canadian Academy of Health Sciences. (2010). Transforming Care for Canadians with Chronic Health Conditions. Retrieved from http://www.cahs-acss.ca/wp-content/uploads/2011/09/cdm-final-English.pdf

15. Public Health Agency of Canada. (2011). Chronic Diseases – Most Significant Cause of Death Globally. Retrieved from http://www.phac-aspc.gc.ca/media/nr-rp/2011/2011_0919-bg-di-eng.php

16. World Health Organization. (2014). Noncommunicable Diseases (NCD) Country Profiles 2014. Retrieved from http://www.who.int/nmh/countries/can_en.pdf?ua=1

17. Public Health Agency of Canada. (2011). Chronic Diseases – Most Significant Cause of Death Globally. Retrieved from http://www.phac-aspc.gc.ca/media/nr-rp/2011/2011_0919-bg-di-eng.php

18. Health Council of Canada. (2012). Self-management support for Canadians with chronic health conditions. Retrieved from http://www.selfmanagementbc.ca/uploads/HCC_SelfManagementReport_FA.pdf

19. Elmslie, K. (n.d.) Against the Growing Burden of Disease. Retrieved from http://www.ccgh-csih.ca/assets/Elmslie.pdf

20. Public Health Agency of Canada. Chronic Diseases – Most Significant Cause of Death Globally.

21. Canadian Academy of Health Sciences. Transforming Care for Canadians with Chronic Health Conditions.

22. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

23. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

24. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

25. Canadian Institute for Health Information. (2011). Primary Health Care information Sheet. Seniors and the healthcare system: What is the impact of multiple chronic conditions? Retrieved from http://www.cihi.ca/CIHI-ext-portal/pdf/internet/info_phc_chronic_seniors_en

26. Canadian Institute for Health Information. Seniors and the healthcare system.

27. Canadian Institute for Health Information. Seniors and the healthcare system.

28. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

29. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

30. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

31. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

32. Canadian Institute for Health Information. (2013). National Health Expenditure Information Sheet. Health spending in 2013. Retrieved from http://www.cihi.ca/CIHI-ext-portal/pdf/internet/NHEX_INFOSHEET_2013_EN

33. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

34. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

35. Macdonnell, M. & Darzi, A. (April 2013). A key to slower health spending growth worldwide will be unlocking innovation to reduce the labor-intensity of care. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23569044

36. Macdonnell, M. & Darzi, A. A key to slower health spending growth worldwide will be unlocking innovation to reduce the labor-intensity of care. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23569044

37. Macdonnell, M. & Darzi, A. A key to slower health spending growth worldwide will be unlocking innovation to reduce the labor-intensity of care. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23569044

38. Macdonnell, M. & Darzi, A. A key to slower health spending growth worldwide will be unlocking innovation to reduce the labor-intensity of care. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23569044

39. Macdonnell, M. & Darzi, A. A key to slower health spending growth worldwide will be unlocking innovation to reduce the labor-intensity of care. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23569044

40. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

41. Canadian Institute for Health Information. National Health Expenditure Trends, 1975 to 2013.

42. Value-Based Health Care Delivery. (2012).

43. Accenture. (2012). Connected Health: The Drive to Integrated Healthcare Delivery. Retrieved from http://www.himss.eu/sites/default/files/Accenture-Connected-Health-Global-Report-Final-Web.pdf

44. Health Progress. (2013). U.S. Health Care Is Moving Upstream.

45. CancerCare Manitoba. (2014). BreastCheck Mobile Screening Sites. Retrieved from http://www.cancercare.mb.ca/home/prevention_and_screening/public_screening/breastcheck/screening_locations/mobile_screening/

46. Health Affairs. (2002). The case for more active policy attention to health promotion.

47. Health Progress. (n.d.). U.S. Health Care Is Moving Upstream.

48. Ubelacker, Sheryl. (March 2011). MDs can better detect white-coat syndrome with automated blood-pressure devices. Toronto Star. Retrieved from http://www.thestar.com/life/health_wellness/2011/03/15/mds_can_better_detect_whitecoat_syndrome_with_automated_bloodpressure_devices.html

49. Stephenson, D. SAP. (2014). Seniors and the Internet Of Things: Empowerment and security. Retrieved from http://blogs.sap.com/innovation/industries/seniors-and-the-internet-of-things-empowerment-and-security-01249245?campaigncode=CRM-XM14-TH1-CAMOBNAD

50. American Diabetes Association. (June 2014). American Diabetes Month. Retrieved from http://www.diabetes.org/in-my-community/american-diabetes-month.html

51. Curry, N. & Ham, C. The King’s Fund. (2010). Clinical and service integration. Retrieved from http://www.kingsfund.org.uk/publications/clinical-and-service-integration

52. Bodenheimer, T. (2002). Improving primary care for patients with chronic illness. Journal of the American Medical Association.

53. Institute for Competitiveness & Prosperity. (2014). Building Better Health Care. Retrieved from http://www.competeprosper.ca/uploads/WP20_BetterHealthCare_FINAL.pdf

54. Institute for Competitiveness & Prosperity. (2014). Building Better Health Care. Retrieved from http://www.competeprosper.ca/uploads/WP20_BetterHealthCare_FINAL.pdf

55. Centers for Medicare & Medicaid Services. (2012). Initiative to Reduce Avoidable Hospitalizations Among Nursing Facility Residents. Retrieved from http://innovation.cms.gov/initiatives/rahnfr/

56. Mills, C. & Penney, L. (2013). The Northland emergency meningococcal C vaccination programme. New Zealand Medical Journal. Retrieved from http://www.ncbi.nlm.nih.gov/pubmed/23797074

57. Free, C. et al. (2011). Smoking cessation support delivered via mobile phone text messaging (txt2stop): a single-blind, randomized trial. The Lancet. Retrieved from http://www.thelancet.com/journals/lancet/article/PIIS0140-6736(11)60701-0/fulltext

58. Edwards, H., Gibb, M. & Finlayson, K. (2010). Innovations in the care of leg ulcer patients in Australia. Wounds International. Retrieved from http://www.woundsinternational.com/practice-development/innovations-in-the-care-of-leg-ulcer-patients-in-australia

59. Saxe-Custack, A. & Weatherspoon, L. (2013). A patient-centered approach using community-based paraprofessionals to improve self-management of Type 2 diabetes. American Journal of Health Education.

60. McNamara et al. (2013). Early admission to community-based palliative care reduces use of emergency departments in the ninety days before death. Journal of Palliative Medicine.

61. Government of Ontario. (2012). Ontario’s Action Plan for Health Care. Retrieved from http://www.health.gov.on.ca/en/ms/ecfa/healthy_change/docs/rep_healthychange.pdf

62. Champlain LHIN. (2010). Rethinking Healthcare for the 21st Century. Retrieved from http://www.champlainlhin.on.ca/uploadedFiles/Home_Page/Integrated_Health_Service_Plan/EN%20Rethinking%20Healthcare.pdf

63. Hébert, P. (2010). Measuring performance is essential to patient-centred care. Canadian Medical Association Journal. Retrieved from http://www.cmaj.ca/content/early/2010/01/25/cmaj.100053.full.pdf

64. Ontario Telemedicine Network. (2013). Embarking on the Journey for Virtual Care. Retrieved from http://otn.ca/sites/default/files/otn-annual-report-2012-13.pdf

65. PwC. (2014). Making Care Mobile. Retrieved from http://www.pwc.com/ca/en/healthcare/publications/pwc-virtual-health-making-care-mobile-canada-2013-11-en.pdf

66. The King’s Fund & Nuffield Trust. (2012). Integrated care for patients and populations: Improving outcomes by working together. Retrieved from http://www.networks.nhs.uk/nhs-networks/common-assessment-framework-for-adults-learning/archived-material-from-caf-network-website-pre-april-2012/documents-from-discussion-forum/IntegratedCarePatientsPopulationsPaper-KingsFundNuffieldTrust2011.pdf

67. Institute for Competitiveness & Prosperity. (2014). Building Better Health Care. Retrieved from http://www.competeprosper.ca/uploads/WP20_BetterHealthCare_FINAL.pdf

68. Canada Health Infoway. (2013). The emerging benefits of electronic medical record use in community-based care. Retrieved from http://www.pwc.com/ca/en/healthcare/publications/pwc-electronic-medical-record-use-community-based-care-report-2013-06-en.pdf

69. eHealth Ontario. (2014). Progress Report. Retrieved from http://www.ehealthontario.on.ca/en/progress-report

70. McKinsey & Company. (2013). The big-data revolution in healthcare. Retrieved from http://www.mckinsey.com/insights/health_systems_and_services/the_big-data_revolution_in_us_health_care

71. Canada Health Infoway & CIHI. (2013). Better Information for Improved Health: A Vision for Health System Use of Data in Canada. Retrieved from http://www.cihi.ca/CIHI-ext-portal/pdf/internet/hsu_vision_report_en

72. Canada Health Infoway & CIHI. Better Information for Improved Health.

73. Graber, M.L. et al. (2005). Diagnostic error in internal medicine. Archives of Internal Medicine.

74. Canada Health Infoway & CIHI. Better Information for Improved Health.

75. Ontario Ministry of Finance. (2012). Commission on the Reform of Ontario’s Public Services. Retrieved from http://www.fin.gov.on.ca/en/reformcommission/chapters/ch5.html

76. Institute for Competitiveness & Prosperity. (2014). Building Better Health Care. Retrieved from http://www.competeprosper.ca/uploads/WP20_BetterHealthCare_FINAL.pdf

77. Deering, M.J. (2013). Issue Brief: Patient-generated health data and health IT. Retrieved from http://www.healthit.gov/sites/default/files/pghd_brief_final122013.pdf

78. HMcKinsey & Company. The big-data revolution in healthcare. Retrieved from http://www.mckinsey.com/insights/health_systems_and_services/the_big-data_revolution_in_us_health_care

79. Accenture. (2012). Connected Health: The Drive to Integrated Healthcare Delivery. Retrieved from http://nstore.accenture.com/acn_com/PDF/Accenture-Connected-Health-Global-Report-Final-Web.pdf

80. Accenture. (2012). Connected Health: The Drive to Integrated Healthcare Delivery. Retrieved from http://nstore.accenture.com/acn_com/PDF/Accenture-Connected-Health-Global-Report-Final-Web.pdf

81. McKinsey Global Institute. (2011). Big data: The next frontier for innovation, competition, and productivity. Retrieved from http://www.mckinsey.com/insights/health_systems_and_services/the_big-data_revolution_in_us_health_care

82. PharmaTimes Online. (2005). New data up Vioxx heart attack estimates. Retrieved from http://www.pharmatimes.com/Article/05-01-26/New_data_up_Vioxx_heart_attack_estimates.aspx

The Connected World Market Insights Series

The Connected World Market Insights Series will cover such topics as:

- Advanced metering infrastructure (AMI) and smart meters: Building upon a home advantage

- Automation and energy: Unlocking home and building energy management opportunities

- Entertainment for the connected home

- Security: Privacy, data ownership and data risk

- Transforming health: Decentralized and connected care

- Connected mining opportunities and new technologies

- The value of real-time meter data

We’ll highlight the innovators in industry, academia and government throughout this series. In fall 2014, we will cap the series with HomeConnect 2014. This event will feature some of our companies, alongside major industry players, as they showcase their technology and solutions.

Accessing data is key, but we think that being able to format and analyze that data is where the real value can be found. During this series, MI will delve into the market opportunity now becoming available due to progress in opening up datasets, and the development of infrastructure and analytics that are creating new services and products and bringing them to market.